Risk Premium Explained: Stunning Guide to Best Returns

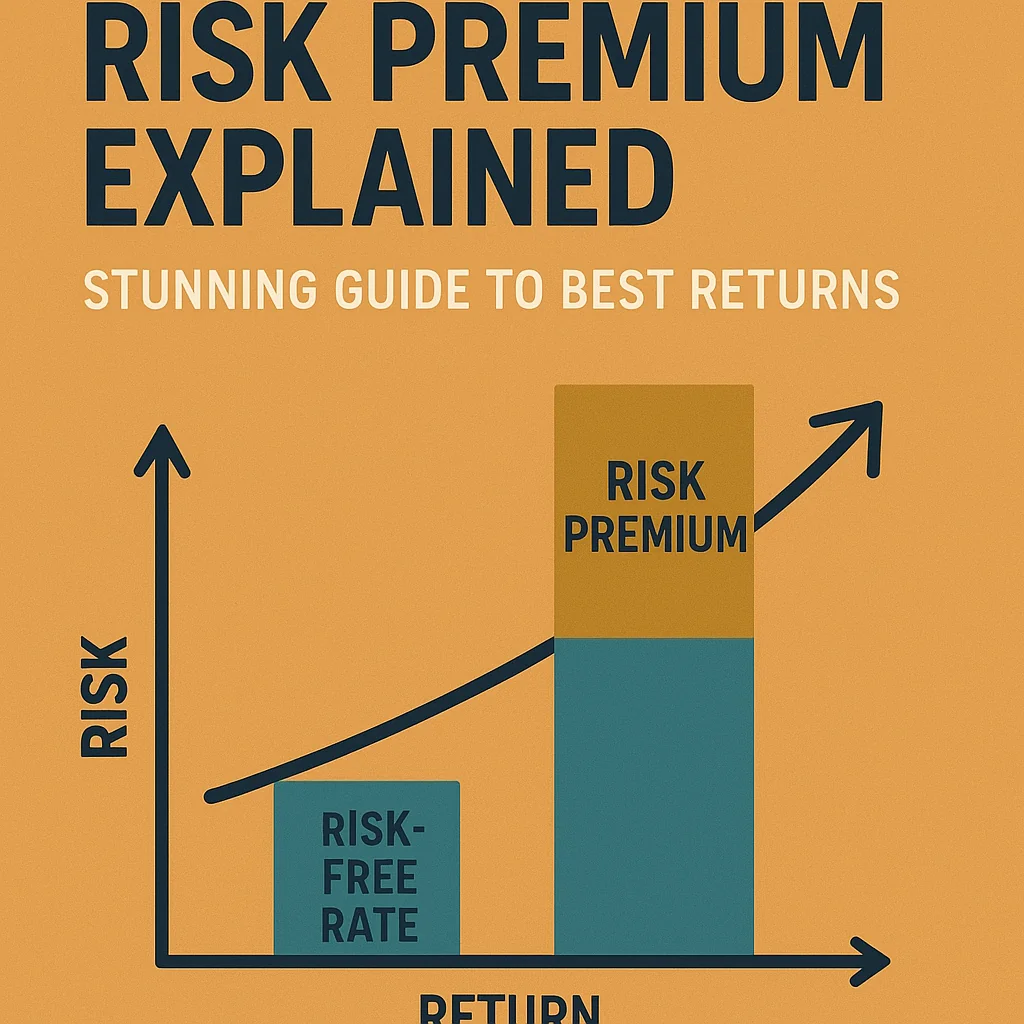

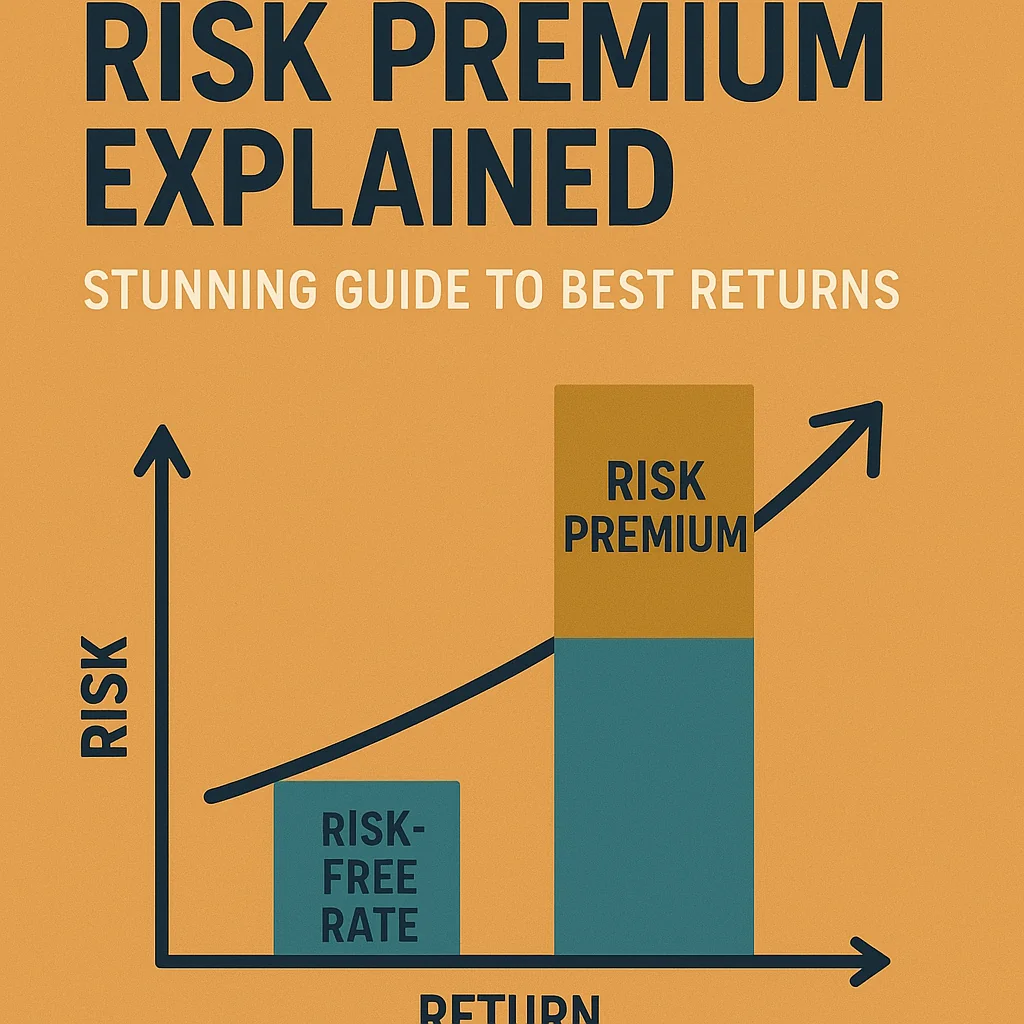

Risk premium is the extra return investors expect as compensation for taking on additional risk compared with a “safe” investment. It is the price of uncertainty. If an asset is riskier, investors demand a higher premium to hold it.

Understanding risk premium helps you judge whether an investment return is fair for the risk you accept. It also helps explain why some assets pay more over time and why others stay relatively low-yield but safer.

Basic Definition of Risk Premium

In simple terms, risk premium is the difference between the expected return on a risky asset and the return on a risk-free asset. The risk-free asset is usually a government bond from a stable country, used as a benchmark.

If a stock is expected to return 9% per year and the risk-free rate is 3%, the risk premium on that stock is 6%. That 6% is what investors want in exchange for the chance that the stock may fall or even lose much of its value.

How Risk Premium Is Calculated

The core idea behind risk premium is simple: subtract the risk-free rate from the expected return. The main challenge is estimating the expected return and choosing the right risk-free rate.

Risk Premium Formula

The basic formula for risk premium is straightforward and used across finance.

Risk Premium = Expected Return of Risky Asset − Risk-Free Rate

A quick example shows how this works in practice:

- You estimate a stock portfolio will return 8% per year over the long term.

- Current 10-year government bonds yield 2% per year.

- The risk premium on that portfolio is 8% − 2% = 6%.

That 6% is what you earn for accepting stock market ups and downs instead of holding only safe bonds.

Expected vs. Historical Returns

Expected returns are often based on history. Analysts look at long-term data to get a realistic range, not just a single number. For example, if global stocks have delivered about 6–7% above inflation over many decades, an investor may use a similar number for expected equity risk premium.

Still, history does not guarantee the future. Some years will be far better, and some far worse. This gap between expectation and reality is exactly why risk premium exists.

Main Types of Risk Premium

Risk premium is not a single number. It appears in different forms across asset classes and specific risks. Each type pays investors for taking on a different source of uncertainty.

1. Market (Equity) Risk Premium

The equity risk premium is the extra return from stocks over the risk-free rate. It rewards investors for stock price volatility, business cycles, and the chance of permanent loss.

For example, if long-term stocks return 10% and long-term government bonds return 4%, the equity risk premium is 6%. This premium explains why retirement portfolios often include stocks despite short-term drops.

2. Credit (Default) Risk Premium

Credit risk premium is the extra yield paid by corporate or high-yield bonds compared with government bonds. It compensates investors for the chance the issuer fails to pay interest or repay principal.

Suppose a stable government bond pays 3% and a corporate bond with similar maturity pays 5%. The credit risk premium is 2%. That 2% is what investors demand for the possibility that the company misses payments or gets downgraded.

3. Liquidity Risk Premium

Liquidity risk premium rewards investors for holding assets that are harder to sell quickly at a fair price. Property, thinly traded small-cap stocks, and some private investments often carry this premium.

An investor might receive a higher yield from a rarely traded bond than from a similar, highly traded bond. The extra yield reflects the risk of getting stuck in the position during stress or selling at a discount.

4. Country (Sovereign) Risk Premium

Country risk premium appears in markets with political, economic, or legal uncertainty. Investors demand extra return for holding assets in countries with unstable policies, weaker institutions, or higher inflation risk.

For instance, a government bond from a stable country may yield 2%, while a bond from a country with higher default risk may yield 8%. The 6% gap includes a large country risk premium.

5. Size and Other Factor Premiums

Academic research points to additional risk premiums, often called factor premiums. Examples include:

- Size premium: Extra return from small-cap stocks compared with large-cap stocks.

- Value premium: Extra return from undervalued stocks compared with high-growth stocks.

- Momentum premium: Extra return from stocks that have performed well recently.

These premiums reward exposure to specific patterns in markets, and they come with their own periods of underperformance and stress.

Risk Premium Examples in Practice

A few simple scenarios make the idea more concrete. Each case shows how investors trade off safety for extra return.

| Asset Type | Expected Return | Risk-Free Rate | Risk Premium | Main Risk Compensated |

|---|---|---|---|---|

| Large-cap stock index | 9% | 3% | 6% | Market volatility |

| Investment-grade corporate bond | 4.5% | 3% | 1.5% | Credit/default risk |

| High-yield (junk) bond | 8% | 3% | 5% | High default risk |

| Emerging market government bond | 10% | 3% | 7% | Country and currency risk |

| Private equity | 14% | 3% | 11% | Illiquidity and business risk |

These numbers are illustrative, not current market quotes, but they show the pattern: higher risk tends to come with higher expected premium, though outcomes can still differ from expectations by a wide margin.

Why Risk Premium Matters to Investors

Risk premium shapes portfolio design, discount rates, and even company valuations. Knowing how it works helps you avoid both underestimating and overestimating risk.

Portfolio Construction

Every investment choice involves trading safety for expected premium. A retiree may choose more bonds and accept a lower risk premium. A young professional may choose a higher share of stocks and accept more volatility for a larger premium.

Over time, the mix between safe assets and risky assets defines how much risk premium a portfolio targets and how much short-term fluctuation the investor must tolerate.

Valuation and Discount Rates

Analysts use risk premium to estimate discount rates in valuation models. A higher risk premium leads to higher discount rates, which reduce the present value of future cash flows and lower estimated fair value.

For example, if a company’s cash flows look uncertain, an analyst will apply a larger equity risk premium to discount those cash flows. That results in a lower target price compared with a stable company with similar cash flows.

Key Drivers of Risk Premium

Risk premiums move over time. They respond to both economic conditions and investor behavior. Understanding the main drivers helps you interpret market shifts with more clarity.

Some of the most common drivers include:

- Economic outlook: Recessions or crises often push risk premiums up as investors become cautious.

- Interest rates: Higher risk-free rates can compress or widen spreads depending on expectations.

- Inflation expectations: Uncertain or rising inflation can increase risk premiums, especially on long-term assets.

- Market sentiment: Fear and stress typically increase premiums; optimism often pushes them down.

- Default rates and credit quality: Rising defaults usually increase credit risk premiums.

In a crisis, investors may rush into government bonds, drive their yields down, and force risk premiums on stocks and corporate bonds sharply higher. The reverse can happen during calm periods.

Risk Premium vs. Risk

Risk premium and risk are related but not identical. Risk is the chance of loss or volatility. Risk premium is the extra return you expect in exchange for that chance.

Two assets can have similar risk but different premiums if investors view their risks differently. Investor demand, regulation, and market structure all affect the premium, not just the raw probability of loss.

How Investors Use Risk Premium in Decisions

Risk premium acts as a benchmark. It helps you decide whether an investment offers enough potential return for the risk you will carry.

Practical Steps to Apply Risk Premium

A simple, structured approach helps keep decisions consistent and less emotional when markets move sharply.

- Identify the reference risk-free rate. Often this is a government bond yield with a maturity that matches your investment horizon.

- Estimate the expected return. Use long-term data, current yields, and realistic assumptions rather than short-term performance.

- Compute the implied risk premium. Subtract the risk-free rate from the expected return to see what premium you are targeting.

- Compare across options. Check if higher premiums come with risks you understand and accept, such as illiquidity or higher default risk.

- Align with your risk capacity. Match the level of risk premium to your time horizon, income stability, and emotional tolerance for losses.

Simple checks like these can prevent decisions based only on headline yields, which may hide credit, currency, or liquidity risks behind an attractive number.

Limits and Misconceptions About Risk Premium

Risk premium is a useful tool, but it is not a guarantee. Higher expected premiums do not promise higher returns in every period. Markets can stay irrational longer than investors expect, and risk can cluster in time.

A common misconception is that any high yield is automatically a sign of a good risk premium. Sometimes a high yield is a warning signal that the market expects trouble, such as a pending default or severe dilution. Another mistake is to focus only on one type of risk, like price volatility, and forget about liquidity or concentration risk.

Summary: What Risk Premium Really Tells You

Risk premium is the extra return you demand to accept uncertainty instead of complete safety. It appears in stocks, bonds, property, and alternative assets, and it responds to economic shifts and investor sentiment.

Used with discipline, risk premium helps you:

- Judge if a return is fair for the risk level.

- Compare different asset classes on a consistent basis.

- Build a portfolio that matches your time horizon and comfort with losses.

- Understand why safer assets usually pay less over time.

The core trade-off stays the same: more risk, more expected premium, but also more uncertainty. Clear awareness of that trade-off is one of the most valuable tools an investor can have.